SEPTEMBER 23, 2016

- The case for staying the course with stocks was bolstered following the FED’s ongoing pause.

- As earnings season arrives, technology to power Nasdaq Higher.

- October can see stock market gains interspersed with sharp volatility from swings in election forecast.

- November is favorable, but generally driven by the election outcome.

“Investors should consider staying the course and maintaining their exposure to stocks. That strategy since March 2016 has served us well.”

The above excerpt from our earlier article, Staying The Course! Stocks Remain Attractive, remains a prudent strategy following the Federal Reserve ((FED)) action earlier this week. Stay invested in stocks.

Federal Reserve has Spoken

The FED Governors at the FOMC meeting left the Federal Funds rate unchanged, providing a runway of clarity for the bond and stock market, at least for the near-term.

The FED message is that accommodative policy remains the preferred choice at this point, given the weakness in near-term economic data. Faced with multiple key economic data points suggesting slower growth – GDP, ISM surveys, business spending – highlighted in the previous article, we believe the FED’s action was a prudent choice.

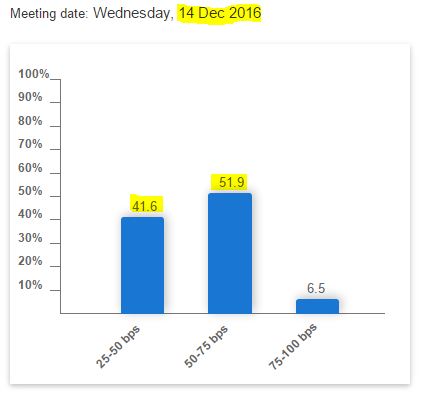

The rate hike debate has now been pushed out towards the end of the year. The chance of any change at the November 2 meeting is highly remote. The next opportunity for a rate hike will be at the December 14 meeting, and that is the date around which the market consensus is now coalescing. In fact, for the first time this year, the Change Consensus (52%) is higher than the No Change Consensus (42%).

We believe that, ((a)) in the absence of any political upheaval in the November elections, which can create a fog of uncertainty around economic policy and consequently jolt the financial markets, and ((b)) with the economic data beginning to ameliorate over the interim period, a December rate hike will be tough to avoid.

Probability of Interest Rate Rise - Consensus View | Source: CME Group

What Does it Mean for the Financial Markets?

Stocks, Bonds and Commodities rallied as it became clear that the FED will remain patient with its accommodative policy, and continue providing the easy money stimulus to enhance economic growth.

Global markets were also mindful of the fact that a patient FED stance, inspite of a steadier economy, exerts pressure on the ECB and BOJ to continue with the stimulative policies for their moribund economies. No wonder the global markets joined the rally to celebrate a continuation of accommodative global monetary policy for at least the near-term.

With the Federal Reserve policies now shifting into the background, the focus in the US will return to the third-quarter earnings, which will pick up pace in the second-half of October.

We believe the market is shifting from a FED-driven market to an earnings-driven one. This will provide fresher legs to the stock market to move higher during October. A threat to our expectation of rising stocks next month is the US election related uncertainty during October, which will intersperse market gains with sharp volatility spurred by the fickle polling predictions of the US elections.

The Nasdaq (QQQ), which once again made a new all-time high following the FED decision on September 21, has had a very strong third quarter so far. The boost in its performance came from the Technology ((Tech)) sector, which delivered promising second quarter earnings and contribute meaningfully to a rise in Nasdaq.

We believe the Tech sector will once again deliver strong earnings growth for the third quarter.

Capital Spending to Benefit Technology Sector

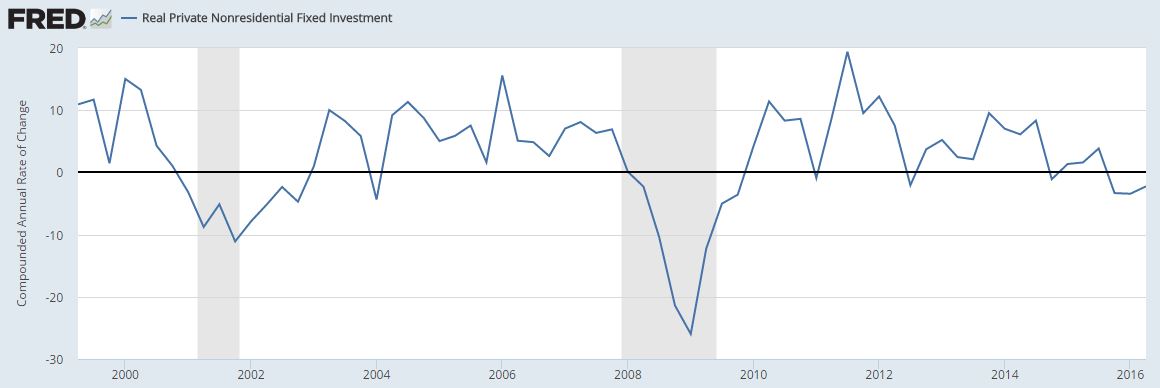

Here's our broader argument for a better Tech performance. Consistent Nonfarm Payroll Growth of 150,000 to 200,000 new jobs cannot occur in a vacuum, without business investment spending eventually turning around with a lag. As can be observed from the chart below, Private Nonresidential Fixed Investment growth has been sub-par in this recovery. After a decline of -2.2% in the second quarter of 2016, it has now dropped in four of the last five quarters.

Source: Federal Reserve Bank of Saint Louis

We believe due to present election uncertainty, the quarterly business spending measure will remain flat-to-down over the remainder of 2016. But most likely the measure will begin to move higher next year once there is political as well as economic-policy clarity.

Since Technology is at the leading edge of this business investment spending, it will continue to be an early beneficiary of corporate spending. Consequently we anticipate the sector to once again outperform its earnings expectations for the third quarter.

The S&P 500 (SPY) should as well benefit from a Technology surge with 21% exposure to Information Technology. However, Energy, which accounts for a 7% exposure, may somewhat drag the performance unless there is an artificial capping of oil supplies through an agreement between major oil producing countries.

Smallcaps will also be a strong beneficiary in an environment of risk-taking, and we anticipate the Russell 2000 (IWM) to make an all-time high during October.

Conclusion

US Elections will now cast a longer shadow over the stock market and guide its direction. Overall, stocks are well-positioned to advance their gains during October and November, provided there are no election related surprises. During the final month of the year, December, we believe investors should be relatively more cautious if an interest rate increase is highly likely. We will consider this framework to guide our investing, but our models eventually decide on our portfolio exposure and allocation.At this time, we continue to maintain full portfolio exposure to stocks. Besides the typical technology stocks that continue to be promising, including Facebook (FB), Amazon (AMZN), Netflix (NFLX), Alphabet (GOOG) (GOOGL), Intel (INTC), Micron Technology (MU), Netapp (NTAP), Microsoft (MSFT), Adobe (ADBE), Sap (SAP), Red Hat (RHT), Momo (MOMO), Weibo (WB), Netease (NTES), Alibaba (BABA), and Sina (SINA), there is a lot happening in Healthcare now. Even Biotechnology has finally begin to emerge from a long slump, with positive trial results, drug approvals, and acquisition activity serving as catalysts. There are a number of promising names including Amgen (AMGN), Seattle Genetics (SGEN), Merck (MRK), Incyte (INCY), Exelis (EXEL), Nektar (NKTR), Ariad (ARIA), Medivation (MDVN), Exact Sciences (EXAS), Bluebird Bio (BLUE), Tesaro (TSRO), Sarepta Therapetics (SRPT), and Clovis (CLVS), to name a few.

If you wish to add to this article or share your viewpoint, please leave a Comment for everyone's benefit. Thanks!

The article can also be viewed on Seeking Alpha.